My friends at Pakdi.net recently wrote two brilliant articles about monthly budgeting.

The first one was written from the perspective of an enthusiastic (though slightly delusional) fresh graduate who earns RM 3,500 (~833 USD). He starts planning his budget with a new car and a generous portion for eating out — only to discover that RM 3,500 isn’t enough for him. What to do?!

The second one posted a more realistic budget, after receiving tons of comments from readers.

I loved it.

So much, that for the benefit of you guys, I decided to translate some of the article into English, and provide commentary of my own.

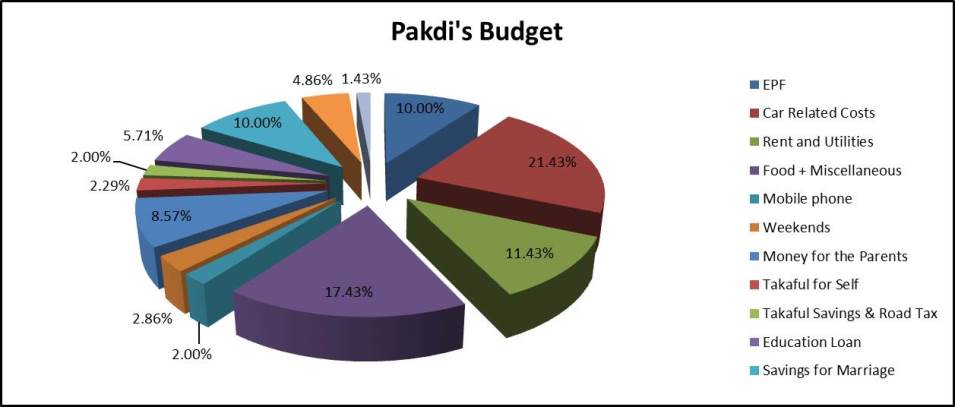

Here’s what Pakdi recommends for a single person earning RM 3,500 in Kuala Lumpur today:

1. Employees Provident Fund (a.k.a. KWSP)

RM 350

No choice here. Mandatory contribution to the EPF.

(And yes, for all you anal people, the actual amount is 11%, plus another RM 14.75 for SOCSO, but let’s not get into too much detail here)

2. Car-Related Costs

A second-hand 2011 Perodua Viva, worth RM 20,000.

Glad I’m not the only one who believes in second-hand cars!

Car loan: RM 300

Petrol and toll: RM 150

Car maintenance: RM 100

Parking: RM 200

Total: RM 750

3. Rent

RM 400 for a single room.

4. Food

RM 2 per day for a simple breakfast = RM 60

RM 10 per day for “food court” lunch = RM 300

RM 150 per month for dinner groceries.

Ugh! Personally, I hate the hassle of cooking. But if you’re on a budget…

Total: RM 510

5. Mobile Phone

RM 70 for a reasonable data plan.

That brand-new iPhone 6S might have to wait…

6. For the Weekends

RM 100

You don’t really need very much, if you spend a lot of time at home on the Internet like me.

7. Personal Miscellaneous Expenses

RM 100

A guy’s gotta look good too!

Total So Far: RM 2,280

Remainder: RM 1,220

Which can now be used for:

- Giving to parents: RM 300

- Takaful (Insurance) for self: RM 80

- Takaful Savings and Car Road Tax: RM 70

- Education Loan: RM 200 (be responsible!)

- Savings for marriage!: RM 350

- Investments: RM 170

- Savings for holidays: RM 50

Does this sound like a reasonable budget to you?

In percentages

In percentages

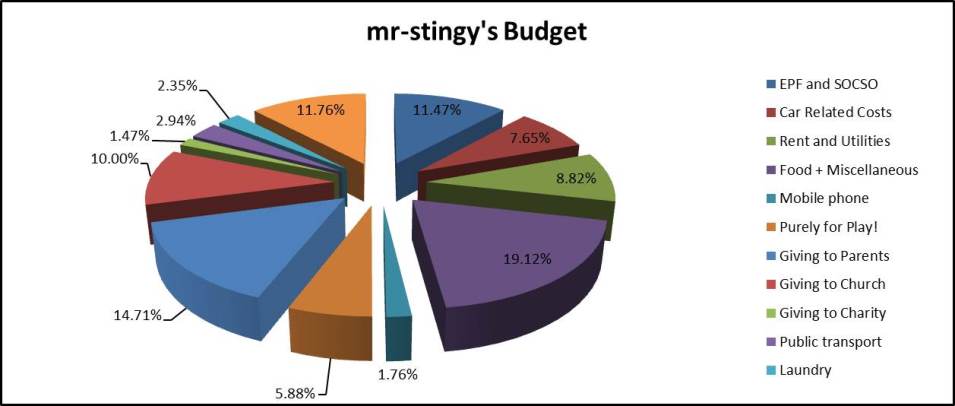

For comparison’s sake, I decided to look at my personal budget from 2010. This is what I found:

mr-stingy’s Budget from 2010 — back when he wasn’t called mr-stingy

Basic Salary: RM 3,400

- EPF and SOCSO: RM 390

- Tax: RM 70 (Yes, back in 2010, you were already getting monthly tax deductions on RM 3,400 salary)

- Rent and utilities: RM 300

- Giving to church: RM 340 (the Christian equivalent of Zakat)

- Giving to parents: RM 500

- Giving to charity: RM 50

- Car petrol and maintenance: RM 260 (I was lucky enough to have an old car to use, without having to pay for a loan. Thanks Dad!)

- Public transport: RM 100

- Laundry: RM 80 (Sorry, I’m too lazy to do my own laundry)

- Mobile phone: RM 60

- Food & miscellaneous: RM 650

- Savings and investment: RM 400

- Purely for play!: RM 200

As you can tell, marriage isn’t high on my priority list

As you can tell, marriage isn’t high on my priority list

If I could do it over again, I would make the following adjustment:

- Increase savings and investments, and reduce food

That being said, I think it was an OK budget for me at that time. I led a very happy, carefree life.

Of course, everyone’s budget is going to be different. It really depends on your priorities (e.g. whether you want to retire young, if you wanna get married asap, or if you’re lazy like me). But hopefully the two budget examples above can give young people some ideas on how to allocate their money.

Remember — most working adults don’t have a budget for their monthly spending. If you’d like to become the master of your money, I highly recommend you start.

Finally, if you’d like to know my personal tips on how to set a budget, click here.

What do you think about the two budgets above? Are they realistic in this day and age? I’d love to hear your tips and thoughts.

Thanks Pakdi for letting me reuse your valuable information.

Picture at Pexels.

Thanks for the great article!

My first salary started from 2.5k 4 years ago. Even so, I managed to save a good 30-40% each month without knowing the golden rule of pay myself first. Eventually with each increment in salary, my lifestyle inflation increased tremendously too; I signed up for gym membership that I don’t always go, I went out dining more often with better choices of restaurants etc…

This year, I revised the way I use my salary and “reset” my lifestyle inflation. I am now proud to say that I am saving min 60% a month by paying myself first!

Thanks Cheryl for dropping by.

Saving 60% per month is not easy at all. You’re well on your way to early retirement!

My jaw dropped at the savings rate. And here I am using every tricks in the book to save a measly 21%. Sad emoticon

Mr. Money Mustache says here that if you save 60% of your salary, you can retire in 12.5 years.

http://www.mrmoneymustache.com/2012/01/13/the-shockingly-simple-math-behind-early-retirement/