“Save money” is perhaps the most common piece of advice of all time. Most of us know that it’s the right thing to do. And yet, a lot of us don’t do it.

Have you ever wondered why?

I think I might have found the answer.

Maybe it’s because saving small amounts of money can feel worthless.

I know — because I used to feel that way too. Back when I first started work, I earned a grand total of RM 2,510 (~USD 627) per month. After deductions, my take-home salary was about RM 2,220.

I never saved any money. Not because I didn’t know about personal finance. Only partly because I had bad discipline. But a big reason was I didn’t think that 10% savings (the amount that most financial advisers ask you to start with) was going to make a difference. I would rather spend the money chasing girls.

After all, what can savings of RM 222 a month do?

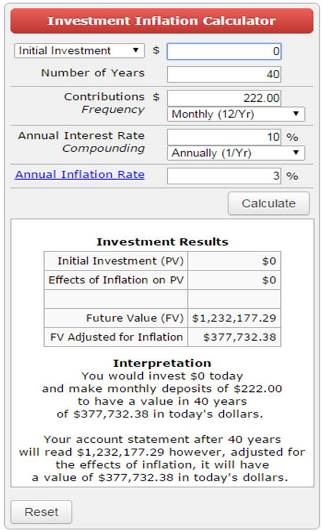

“If you Save RM 222/month and It Returns 10% a Year, by the end of 40 years you’ll have RM 1.2 Million”

The above statement may sound incredible, but it’s absolutely true.

Personal finance advisers will tell you this kinda stuff to encourage you to save money. It illustrates the power of compound interest — if you give it enough time, your money will grow to huge amounts.

“Sikit sikit, lama lama jadi bukit.”

Right. But let’s take a more realistic look at this:

- RM 1.2 million in 40 years’ time isn’t as valuable as RM 1.2 million today. Remember how fifteen years ago a bowl of noodles was only half its price today? Inflation is gonna happen in the future too.

- It’s difficult to consistently get 10% returns for 40 years in a row. To be realistic, I’m gonna say the average investor will do at best what the EPF has been doing for the past few years: around 6%.

(BTW don’t listen to anyone who promises you 10% real returns every year. Either that person is lying, doesn’t know what he’s talking about or is the next Warren Buffet. And even Warren Buffet doesn’t promise you anything)

So our “realistic money” after 40 years looks more like this (assuming 3% inflation):

via Calculator Soup

via Calculator Soup

Three hundred and seventy seven thousand.

Still pretty good. But no longer puts you in the millionaire’s club.

And doesn’t address the burning issue that every young person has…

I Don’t Wanna Wait 40 Years to be Rich!

Right. You wanna buy your luxury bungalow tomorrow. Or at least in the next three years.

I don’t blame you. I wish I could be a millionaire now too.

But I purposely threw out the above paragraph to illustrate something: saving small amounts of money will not make you rich. Let’s do the math: If you need RM 30,000 as downpayment for a new home, and can only save RM 222 a month — it’ll take you around ten years to accumulate that money!

In the meantime, the best your savings will do is provide you backup in case of emergencies.

How discouraging. So why the hell should you save money, if it’s not gonna make you rich?

Why not indulge in hipster coffee, iPhones and new cars instead? Or “invest” in MultiLevel Marketing schemes that promise you easy money?

And then worry about saving only when your salary goes up: “I’ll start saving money once I get that promotion!”

Unfortunately, that’s a terrible idea.

Here’s why.

Habits: If You’re Not Saving Today, You Probably Won’t Save Tomorrow

If you wait to save money — you might never start. Most people increase their spending just as much (or even more) when they earn more money. It’s called lifestyle inflation and looks like this:

Earn RM 2,500, Spend RM 2,600.

Earn RM 5,000, Spend RM 5,500.

Earn RM 10,000, Spend RM 11,000.

Even RM 1 million / month isn’t enough. Before they know it, they’re 40 years old, in serious debt and stuck in a job they hate.

Here’s a statistic that shocked me: some sources say that 70% of people who suddenly receive a lot of money (for example, winning the lottery) finish all the money within 7 years.

We’re talking about millions of dollars here. How do you even finish using that amount of money!? But the sad truth is this: the people who became broke never learned how to manage money properly. They never had the money skills. It was inevitable that they were going to lose it all.

It’s like losing weight. Why do some fat people try all kinds of diets, lose a bit of weight, and then gain it all back again? Because they don’t develop the right habits. They eventually go back to eating unhealthy food and not exercising — it’s inevitable that they become fat again.

If you can’t save even a bit of money when you’re earning RM 5,000*, I’ll bet you won’t save money when you earn RM 50,000.

Your daily habits today determine what your life becomes in 10 years’ time.

* * * * * * * *

The real reason to save money isn’t so that you’ll become rich. It’s so that you develop good financial habits.

That 10 percent may be a small amount in dollars, but it will do wonders for your character. It probably won’t make you a millionaire — but it’ll put you on the right path: the path to financial security.

So remember — even if you’re not able to save a lot of money every month — do it anyway. As much as possible. It might feel like torture, but keep practicing that good habit. Then increase your savings and investments as you start earning more. Train that financial muscle.

And then someday when you earn a lot, you’ll be strong enough to manage all that money well.

And then you’ll be rich.

*I recognize that some extremely poor people have no way to save money at all. These hardcore poor people need external help to break out of the poverty cycle. For the rest of us lucky ones though — I think everyone should be saving at least a bit of their monthly income.

Picture at Pexels

This article first appeared as a guest post at iMoney.

I just lost RM5k for a endo specialist over a broken file in my root canal…I am sad as well which I want to be strong in my financial spending and to find ways to earn back that RM5k which is in my unexpected spending budget =(

Sorry to hear that Moon. Hope you find back your 5k in due time…

blushed ** I am that type of person who would spend more than I earn. gosh, thanks for the reminder.

You’re welcome 🙂

HI Aaron ,

I’m currently a student who are hardworking to earn money from doing part time job earn to paid for my course fees. If i have RM10,000 of my savings what should i do as a students?

Hello KY,

I know too little about your situation to advise. If you like, do give me more details via email, and I’ll see if I have any ideas. Things like what is your current situation, what are your objectives, and your current knowledge level about investment/savings. The more details you have, the better 🙂

My mom told me “How much you can save.is more important than how much you can earn,”

Much fun reading your blog

Happy new year to you.

Irene

Thanks Irene,

Your mom was right. Happy new year and come back for more soon!

Hi Aaron

You are absolutely right! Practicing the good habit. I believe, slowly it’ll also effect the way we manage our daily lives..

Thanks Nana 🙂