An investment portfolio is the mix of things you invest money in. And it’s usually a mix of things because you don’t want all your money stuck in just one thing. For example, if all you invest in is Snapchat shares, guess what happens to your wealth when Kylie Jenner tweets something bad and 51% of the world decides to use Instagram instead?

But how do you decide what goes into your mix of investments?

I recently ran a survey among readers for what you wanted me to write about next. The winner by far was: “How to build your investment portfolio.” So I know there’s a lot of demand out there for investment knowledge. I know it’s important to you guys, because in today’s day and age — it’s so hard to make good money anymore right?

So let’s get straight to it. In this article we’ll look at some common strategies for building investment portfolios. Finally, as a case study, we’ll look at mine; how I’ve built my investment portfolio over time.

But before we dive into technical “how many percent bonds, how many percent stocks?” questions, let’s first take a step back and talk about why investing can (and should) be vastly different for different people.

Investing Is a Very Personal Thing

In an ideal world, we’d all make tons of money from our investments and never lose. The markets would go up forever and we’d sell our RM 58.30 PETRONAS Gas stocks to buy Ferraris.

Alas, the world doesn’t work this way. The markets go up and down, and there’ll always be winners and losers. That’s just capitalism.

But perhaps the more interesting thing is that not everyone wants to drive a Ferrari. Some people would rather go on a food trip to Bangkok. Likewise, most people probably don’t find joy in buying Oil & Gas stocks. Some people would rather invest their money in properties.

So the first thing to understand about investment portfolios is that it’s gonna be different for everyone. Let that message sink in for a while. The 25-year-old management trainee will invest differently from the 40-year-old housewife. And even two 30-year-old accountants might have completely different portfolios.

The great thing is that you get to decide. And you decide based on mainly two things…

Goals and “Risk vs Reward”

What do you want to achieve by investing your hard-earned money? Or rather, what are your financial goals? For example, common goals for young people are saving for your future child’s education, and funding your retirement.

And depending on your goals, the way you invest will be very different. Planning for three kids who’ll go to international schools is different from planning for a single kid who’ll go to government school. Likewise, planning to retire at 60 in a seaside village is worlds apart from a Jho-Low-style retirement in a yacht off the coast of Bali.

Which brings me to a quote I love:

“If you want success, figure out the price, then pay it.”

– Thomas Oppong –

We could all set ambitious goals, but how much are you willing to sacrifice to achieve them?

And the follow-on money question: How much risk are you willing to live with, to get the rewards that you want?

Because if you want higher returns, you’re gonna have to get comfortable with higher risk (i.e. higher chance of losing your money). We’ve all heard of high-risk investors losing their health — and in some tragic cases, their lives — just because they couldn’t handle the stress.

On the other hand, if you want very little risk, your investments are gonna take a really long time to grow. That’s just the law of nature, and despite what 100 ugly skim-cepat-kaya gurus may tell you, there’s no “hack” around it.

Now as your brain contemplates the above philosophical questions, allow me to introduce some common ways to design your investment portfolio.

1. Traditional Strategy: The Stocks-Bonds Ratio

The classic way of designing an investment portfolio is the stocks-bonds ratio. In a nutshell, you decide how many percent of your investments should be in stocks, and how many percent should be in bonds.

BTW, when I say “investment portfolio,” I mean money that you set apart to grow. This doesn’t include “necessities” like your emergency savings (aim for: six months of monthly expenses here) and rent/loans you pay for your home.

So how many percent stocks and how many percent bonds?

120 – [your age] = Percentage of investments in stocks

Let’s say you’re 35 years old. 120 – 35 = 85. So according to this calculation, you should have: 85% invested in stocks, and 15% in bonds.

To further illustrate this:

- Age 25: Stocks 95%, Bonds 5%

- Age 35: Stocks 85%, Bonds 15%

- Age 45: Stocks 75%, Bonds 25%

- Age 55: Stocks 65%, Bonds 35%

- Age 65: Stocks 55%, Bonds 45%

The stocks-bonds ratio is actually an oversimplified principle derived from Modern Portfolio Theory, work which won Harry Markowitz the 1990 Nobel Prize in Economics.

1a. Going Deeper Into Stocks-Bonds

Let’s dive a little deeper now. For example, maybe your target is 80% stocks and 20% bonds. But what stocks and what bonds?

Depending on how hardcore you are, you could end up with a simple and practical portfolio using one ETF and one bond fund:

(Caution: The stocks-bond ratio is based on the behavior of the USA stock market. I’d caution against taking it and literally throwing 85% of your investments into the Malaysian stock market. Ours is a young, emerging market — the USA is a mature one.)

Or, you could end up with a monster like:

- 10% USA blue chip stocks

- 10% USA tech stocks

- 10% Asian blue chip stocks

- 10% Asian value stocks

- 10% Asian REITs

- 10% Malaysian blue chip stocks

- 10% Malaysian value stocks

- 10% Malaysian growth stocks

- 10% Southeast Asian bonds

- 10% Malaysian bonds

Who has time to manage a portfolio like that though? Especially if you’re picking individual stocks. If the above scares you, you’re gonna like Section 2…

(p.s. Check out some nice variations to the stocks-bonds ratio by Vanguard and Financial Samurai.)

Note that in recent years, there have been more and more voices criticizing Modern Portfolio Theory, saying it’s not applicable in our modern world anymore, as compared to say the 1970s to 1980s.

I’m not smart enough to decide whether Nassim Taleb or Harry Markowitz is right, but I am trying to learn from both sides of the argument. We’ll explore my personal investment portfolio in more detail in Section 3.

2. The Advisor Strategy

In this strategy, you outsource your investment decisions to a personal finance advisor. Now if you’ve been reading my articles for a while, you know I like to DIY my money decisions. So this isn’t my preferred way of doing things.

But let’s say you’re an Insta influencer/YouTube star with huge earnings; and you don’t care about investment at all. (You really should.) What if you really don’t give a f*ck, and are only interested in where’s the next beach party? Well, if you don’t wanna go bankrupt in a few years, the best move you could make is to hire a smart person to manage your finances.

Sound crazy? Well, some people really don’t have time to manage small details. I’m looking at you highly-paid professionals in the corporate world too. Plus I know how investment feels really daunting for many people — they’d rather not do it themselves. I’d love for you to study money the way I do, but if you don’t want to, maybe hire someone who’s capable?

There’s also another way. And it’s really cool too.

2a. An Advisor Isn’t Necessarily a Human

The good news is that robo-advisors are already on the horizon. These are apps/websites that use artificial intelligence to help you make investment decisions.

Remember the traditional stocks-bonds ratio above? Take that, mix in some other cool investment theories, program it into AI, add a pinch of user-friendliness, and there you have it: advice on how to invest, designed for the average person on the street. And it’s not just advice, robo-advisors literally accept money from you and do the nitty-gritty work of actually investing the money.

This is really cool, but the cooler thing might be this: Because it relies heavily on computers/AI, robo-advisory makes things a lot cheaper for you, the end consumer.

For example, most people are already somewhat familiar with unit trusts. Well, expensive unit trusts in this country charge sales fees of 5% and have annual fees of about 1.5%. Expect robo-advisors to have 0% sales fees, and annual fees between 0.2 to 0.8%. (That’s at least 2-3 times cheaper even before you count the sales fees.)

The expectation is that we’ll have a few robo-advisors launched by end 2018 right here in Malaysia. (Maybe we’ll see some of the popular Singapore-based ones come over.)

Personally, I’m eagerly anticipating this. I’ll likely be moving a chunk of my investments into robo-advisory.

Update Dec 2018: The first robo-advisor to launch in Malaysia is called StashAway. If you’d like to try, they’ve even got a special promo for you, my beloved reader: To get a 50% discount on fees for 6 months, click here.

3. How I Built My Investment Portfolio

The first investment my risk-averse mother ever bought for me was something called Amanah Saham Wawasan 2020. We’re two years away from 2020 and I still have those funds. It’s averaged 6-10% annual returns (and grown 5x) over the past 22 years.

My father is a risk taker and used to play the stock market. One day he sold a stock that’d gone up and bought me my first guitar. 21 years later, I still play at private events sometimes. Thank you Mom and Dad for my first investments.

I believe growing up with parents who had different opinions about money really helped shape the way I invest today. I’m still very careful with my money, but given the right circumstances, I understand the potential of a high-risk investment.

Which is why my investment portfolio looks different from what a traditional finance advisor might recommend. And it looks like this:

3a. mr-stingy’s Investment Portfolio

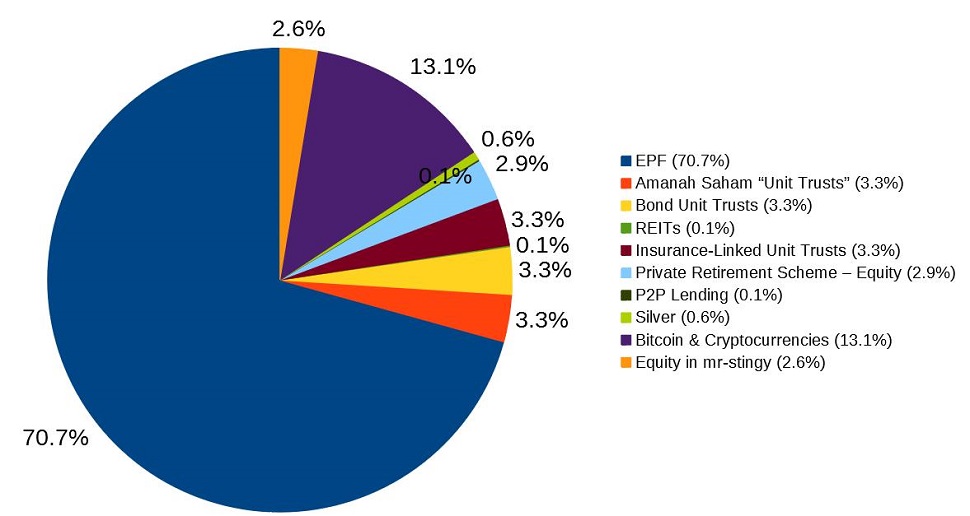

About 80% of my investments are what I’d call “safe”:

- EPF: 70.7%

- Amanah Saham: 3.3%

- Bond Unit Trusts: 3.3%

- Real Estate Investment Trusts (REITs): 0.1%

- Insurance-Linked Unit Trusts: 3.3%

The Malaysian Employees’ Provident Fund (EPF) has declared yearly dividends between 5% to 8.5% every year over the past 50 years. Of course, past returns don’t guarantee what happens in the future — but a little-known fact is by law, the EPF needs to pay yearly dividends of at least 2.5%. It’s as “safe” as you can get in Malaysia. Similarly, fixed-price Amanah Saham funds have never failed to disappoint over the past few decades.

Bond unit trusts and REITs are my other “safe” investments. Though definitely not EPF/Amanah Saham bulletproof, I’m expecting these investments to give me steady dividends over the long run — to protect my capital and fight inflation.

Lastly, I have some money in insurance-linked unit trusts. Like most people my age, I buy investment-linked insurance plans, and a portion of this automatically gets invested into unit trusts.

When I bought these plans, I wanted to force myself to save money, and have some backup in case one day I’m broke and can’t pay for insurance. It’s not the cheapest way of investing (high sales fees!) though, so it’s something I’m reconsidering.

What’s All the High Risk Stuff?

Of course, the 20% is where it gets interesting. These are investments where I’m really hoping to make money:

- Private Retirement Scheme (PRS) – Equity (2.9%)

- P2P Lending (0.1%)

- Silver (0.6%)

- Bitcoin & Cryptocurrencies (13.1%)

- Equity in mr-stingy LLP (2.6%)

My PRS money is invested in equities (stocks) in the Asia Pacific region. Since it’s gonna be decades before I retire, I figure I can afford the higher risk. Even if it goes down at some point, there’s enough time for it to go back up.

Next, Peer-to-peer lending is a really cool new investment. You can get up to 14% returns per year, and the default rate (where the borrower can’t pay you back) is really low. The reason I don’t have more here is because I only recently tried it out, and I’m still very distracted by cryptocurrencies.

On to silver, Bitcoin and cryptocurrencies — my “hedges” in case the financial system as we know it today goes down in flames. Okay, being dramatic here — but these are “backup” if/when the economy crashes next. Also, particularly with Bitcoin, I sincerely believe there’s a chance it still grows 10x or maybe even 20x. Note that even with the recent bloody crash in cryptocurrency prices, I’m still up 53% in less than 2 years in crypto.

Finally, I have a bit of money invested in my own business, mr-stingy LLP. Yeah, I do it for the love, but love costs money too right?

3b. What Do You Call mr-stingy’s Strategy?

Actually, I never planned for my portfolio to be 80% safe and 20% risky. It’s really only this way because for most of my life, I’ve been a conservative investor. Only in recent years have I tried riskier stuff, after being confident I had enough safe assets.

Nassim Taleb writes about investing like a barbell — having lots of safe assets on one side, balanced by a couple of risky assets that could really grow huge. I can’t claim to have followed his strategy exactly, but it’s probably the closest thing to an “investing philosophy” I believe in.

The rationale behind barbells is clear: having most of my investments in safe stuff gives me peace of mind. It gives me confidence that even in the worst economic conditions, I’ll be okay. And the little I have in risky stuff? Well, even if it crashes to zero, I’ll still be fine. But if just one of those investments goes 10x or 20x, that’ll be a huge bonus.

Of course, my investment portfolio is far from perfect. It has a lot of baggage, accumulated from years where I didn’t know better. For example, I always promote passive, low-cost investing (like Warren Buffett). But I still have money in expensive unit trusts. Eventually though, I’m aiming to switch to more-efficient funds like ETFs.

I’ve also probably got too much invested in Malaysian ringgit. When robo-advisors launch here, I’d like to move more into USD assets.

Am I suggesting you should invest like I do? No. But I hope you’ll put as much thought as possible into planning your own portfolio. And in case you’re feeling overwhelmed by all this information, don’t be discouraged — we’re all trying to figure this out as we go along.

What Works for You?

I hope the above perspectives have given you some things to think about. Again, as I mentioned at the start, investing is a deeply personal thing, so I’m not suggesting you invest like me, or directly apply the stocks-bonds ratio. It’s much better for you to think about what we’ve discussed, and then make your own decisions.

I also wanna point out a curious human trait. Back when I first started writing, I believed in the common fallacy that if you just give people better information, they’ll make better decisions.

Well it turns out humans often don’t make decisions rationally. So while I’ll never apologize for writing in-depth 3,000-word articles, I also realize that most people aren’t just gonna read something and suddenly make better decisions.

Which makes me believe that for most people, automating your investments via a robo-advisor makes the most sense. It makes investing cheap, simple, fast, and can be easily customized according to your preferences. You don’t have to spend too much time or effort, and will be able to sleep easily at night.

But in case you’re in the small minority who really likes to get into deep investment things like the Efficient Frontier and 200-day EMAs, allow me to propose a toast to you with my finest virtual glass. In this world of superficial distractions and instant gratification, people who choose the hard route of learning difficult things never fail to inspire me. I’m sure if we ever meet in person, we’ll have lots to talk about.

Until then, may your investments be fruitful.

– – –

Further reading: The Ultimate Guide to 11 DIY Investment Options in Malaysia.

The link to StashAway is an affiliate link: Click for an exclusive 50% discount, and I’ll get a small referral fee too.

Pics from Pexels, Pixabay, Pexels, Pixabay & Pexels.

This is the first article of yours that I have read and I am hooked! Thanks for writing in such a clear and concise manner. Will check out the other articles too.

Thanks Shawn,

Appreciate you dropping by. All the best!

Hello Aaron,

Thank you for your work with Luno.

Would you be able to update this article with your current investment portfolio and why you made those tweaks?

Thanks!

Hi Claudia,

Thanks for dropping by. The latest update on my investment portfolio can be found here: https://www.mr-stingy.com/how-invest-own-money/

Hope it helps!

Hi Mr-Stingy,

Thanks for your article! I’ve started with StashAway bout 3 weeks back with your link to enjoy that 50% discount. Well, I’m ‘cheap’ but I think in a good way. Credit to you too that I start to look at my investment portfolio in serious mode. Thank YOU 🙂

Thanks for dropping by Teng!

Appreciate your support and wishing you the best on your journey!

Hi, Mr.Stingy, can u help me on, how much shall I invest in HelloGold app, to get an monthly income of RM1000

Hi KD,

I think we need to be clear here, investing in Gold does not generate monthly income. It’s not a “cashflow generating” asset that pays you dividends (like stocks and bonds). For monthly income you should look at things that pay you dividends. Just an oversimplified example here: If you want RM 1,000 per month:

– That means RM 12,000 dividends per year

– Assume you’re investing in things that pay 6% per year (not guaranteed btw)

– That means you need to invest 12,000/6% = RM 200,000 in capital.

Dear Mr. Stingy, Can you kindly help to advise a good bond fund? I see in your above article you mention Eastspring Investments Bond Fund. Is it something you recommend? Any other good bond funds? Thanks a lot!

Hi Baymax,

I haven’t looked too deeply into bond funds myself to specifically recommend any. However I do take recommendations for my own personal portfolio from Fundsupermart. Perhaps you can sign up for an account there and have a read about their bond funds?

Thanks for the advice and recommendation, Mr. Stingy. Will check out Fundsupermart. 🙂

All the best!

I really need thi investment and I really appreciate

Thank you!

Hello Mr. Stingy,

I already invest at ASBF Maybank. Do you think it’s okay to invest unit trust (public mutual) but this one is cash?

Hi Farah, I’m not a fan of traditional unit trust companies because of high fees. This article shares you some reasons why: https://www.mr-stingy.com/invest-robo-advisors-malaysia/

Aaron,

What is P2P investment and how do I get into it? Please advise.

Thank you,

Ling

Hi Uncle Ling,

You can find out more details here:

https://www.mr-stingy.com/diy-investment-options-malaysia/

Hey there,

Could I know why you consider P2P a risky investment when the default rate has remained at 1-2%?

As someone who isn’t required to invest in EPF, P2P is my main form of investment (80%+). Do you think that that’s risky?

Hey Ryan,

So the thing about P2P lending is unlike other investments, you could lose your capital. For example, today’s default rate is 1-2%. But say the economy goes through tough times and the default rate shoots up to 10% or 20%. That might mean that 1 out of 5 of your investments is almost completely gone (worst case scenario where they borrower can’t pay back at all).

There are many other “safe” investments where your capital is guaranteed. You won’t ever lose it, but in a bad year you might just get lower dividends or interest. I do think 80% in P2P is very risky, however everyone should measure risk/reward based on their own objectives and standards. Hope this helps!

Hi,

Thank you for your article. It has been very insightful especially for an investment newbie like myself.

I have very limited knowledge on investment. Currently, my only form of investment has been EPF and FD. Thanks to your article, I am trying out StashAway as well.

My question here is:

1) In the range of ‘safe’ and ‘risky’ investment, where do you think StashAway sits?

2) What other ‘safe’ platforms of investment do you recommend? As ASB is rather difficult to obtain for non-Bumi?

Thank you!

Hello Amanda,

Thanks for your kind words. Can refer to my article here for some help: https://www.mr-stingy.com/diy-investment-options-malaysia/

1. StashAway invests purely in ETFs, hence I would call it right in the middle of the spectrum between safe and risky. Note that you can actually decide on how risky your portfolio should be — so you can customize Stashaway to be as risk-free or as risky as you like.

2. Have a look at REITs. They’re basically investing in property, but without the issues of liquidity and annoying stuff like having to find a renter…

very great article. Nice, for Robo advisor category, how do you see Managed Portfolios? It is somewhat like a robo-advisor but already available in Malaysia.

Thanks! Are you referring to the managed portfolios by Fundsupermart? They’re a lot more expensive than robos, so my vote is with robo. Which have already been launched in Malaysia btw.

I appreciate your articles and it’s really eye opening for a bimbo like me. I’ve got a few questions:

1) 70% of your investment comes from EPF. Do you withdraw from your Account 1 to invest in unit trust or other forms of investment? OR it’s pure EPF?

2) I’ve withdrawn from EPF to invest in unit trusts via CIMB Principal and Eastspring. And just realised the amount of sales commission going to them. Should I stop and just let those investments sit OR plough it back to EPF OR move it to ASB?

3) What’s your take on StashAway? And if I want to poke my finger into this pie, what should I do first?

Thanks! And do continue to inspire!

Thanks Chris, really appreciate it. We are all himbos/bimbos at some point in our lives:

1. Nope, I’ve left my EPF untouched since I started working more than a decade ago. When I review how it’s grown I’m actually very happy about it.

2. Disclaimer: not investment advice, but this are my personal thoughts. I don’t really like the idea of moving funds from your EPF to other high-cost investments. As for the money that you’ve already invested, understand you’re probably getting charged 1.6-1.7% per year on management fees. I can’t recall how much ASB charges you — but it should be much lower. Also, ASB’s returns are consistently high. Without knowing too much about how your CIMB and Eastspring investments are doing, I suspect over the long run: ASB will win.

3. IMHO StashAway is great. It allows the average person (who maybe doesn’t have time/interest to study investing so deeply) to invest in a wide range of quality ETFs in the USA market. You can start by reading my article here: https://www.mr-stingy.com/invest-robo-advisors-malaysia/

But more than that, perhaps you can take RM 1 or RM 10 of your money and try it out for yourself. No minimum amount required — so a great opportunity to test and learn!

Hi Mr Stingy

Do you invest in US ETF?

Nice article. 🙂

Hi Lee,

Not directly by myself, but via StashAway yes… 😀

I have bookmarked your post for my future reference. Haha Very insightful especially about Robo-Advisor! Thank you for sharing!

Thanks Nisa — appreciate it!

Got to know a few more investment options after reading your article, very insightful!

One question, may I know if you invest in any properties? Seems like many people nowadays think that property is one of the investments that gain high returns.

Hello Lemonade,

I don’t invest directly into any properties, and only have a very small amount in REITs. I think properties are one of those grandmother wisdom, “if you buy land it will always go up in price!” things, so everyone seems to think it’s a great investment. It’s not my cup of tea though — especially if you ask me to do things like chase for rental/maintain the home.

Good sharing about your personal thoughts on investment portfolio. Personally I believed P2P lending in Malaysia has huge room for growth, recently set the scene in the financial services industry since SC started regulating and issued licences to six P2P lending operators in 2017.

Hey Desmond,

Thanks. I like P2P lending too and I hear it’s growing like crazy.

to make it something less obvious, an option like this: https://www.edelmanfinancial.com/investment-management/for-individuals/what-is-the-edelman-managed-asset-program

– professionally constructed portfolios, so you don’t have to research about EFF

– automatic rebalancing, so you don’t have to monitor too frequently

What do you think?

Hey Heng,

I like the idea. Haven’t investigated too deeply, but looks like a low-cost robo advisor for the USA. I’m looking forward to Malaysian ones launching soon!

What do you think?

There are Malaysian ones, I won’t name here. Only the fees are higher than US, comparatively. With time, we may have an equivalent.

Interesting… are you referring to managed portfolio advisory services that already exist? What’s the difference between these and the robo-advisors that SC is granting licenses to?

Yes. First let’s talk about what they have in common. They are both constructed using diverse geographical and sectorial funds in order to capture market growth, yet mitigate inter-geographical/sectorial/instrument funds flows. The portfolio rebalances its allocations based on some rules and period.

The essential difference is in the instrument they use. Managed portfolios use mutual funds whereas robo-Advisors use ETFs. Mutual funds vs ETFs have their own pros and cons.

One interesting development is that developed markets’ robo-Advisors are starting to offer human ‘advisor-assisted’ options due to their exhausting the DIY market.

Thanks Heng

What do you think about property investment Mr Stingy?

Hey Aimi,

I fall back to the common saying “Houses are for living in, not investing.” I think the property market (especially in today’s era) isn’t great for investing. If you’re looking for capital appreciation, prices haven’t really moved much past few years. If you’re looking for rental, well there’s a whole lot of hassle involved (not that practical for working people, plus it probably reduces your quality of life). If I wanna invest in properties, I’d rather invest in REITs — less hassle.

Hi Mr. Stingy,

Could you tell us more about P2P lending investments?

What is the default rate? So far how many % of ROI are you able to get?

I am interested but this is something new for me.

Hello Curious One,

Default rates are supposedly only around 1%. My investments get back about 14-15% per year. You can find out more details in this article: https://www.mr-stingy.com/diy-investment-options-malaysia/

All the best!

Nice, for Robo advisor category, how do you see Managed Portfolios? It is somewhat like a robo-advisor but already available in Malaysia.

Hope Aaron doesn’t mind me answering this.

Whilst I’m a supporter of fundsupermart and managed portfolio, the returns for managed portfolio has been disappointing so far.

You can see the returns in comparison to its benchmark here

https://www.fundsupermart.com.my/fsm/managed-portfolios/portfolio-materials/factsheets

The similar product in FSM singapore has better returns.

https://secure.fundsupermart.com/fsm/maps/portfolio-materials/factsheets

Stashaway Singapore too is doing better than managed portfolio

https://www.stashaway.sg/how-we-invest

Hey QiQi,

I’ve been a long-time user of FSM, but I don’t really like the idea of their managed portfolio. Basically, they’re adding on another 1% layer of management fees, when you’re already paying the fund manager another 1.5% management fees. Looks like a dual layer management fees to me. Stashaway on the other hand is very much a robo-advisor with much lower fees. I’d go for that instead.

Yes and yes. All portfolios have not enough time to demonstrate their performances in a full economic cycle. And portfolios are always launched with the best backtest intentions. Which is still like driving forwards using the backview mirror.

Fees are definitely on the high side despite accounting for selection, % allocation and rebalancing services.

But in terms of the process of accounting for growth and addressing a variety of possible risks, this manner of investing has a lot more structure and basis behind it.

Great article, especially about investments.

Thanks Jakey!